Blockchain is one of the technologies behind cryptocurrencies such as Bitcoin, which facilitates a peer to peer, decentralized digital cash system granting users full authority over their transactional activity and account balances.

Unlike the classic financial systems, there are no intermediaries in blockchain, thereby prohibiting the modification of transactions.

Aside from crypto, blockchain technology has numerous practical applications. Since its inception, this innovation has been honed for diverse industries, including healthcare and supply chain management, to name a few.

Over the previous years, the potential of blockchain technology has been increasingly acknowledged in an array of fields.

| TERM | DEFINITION |

|---|---|

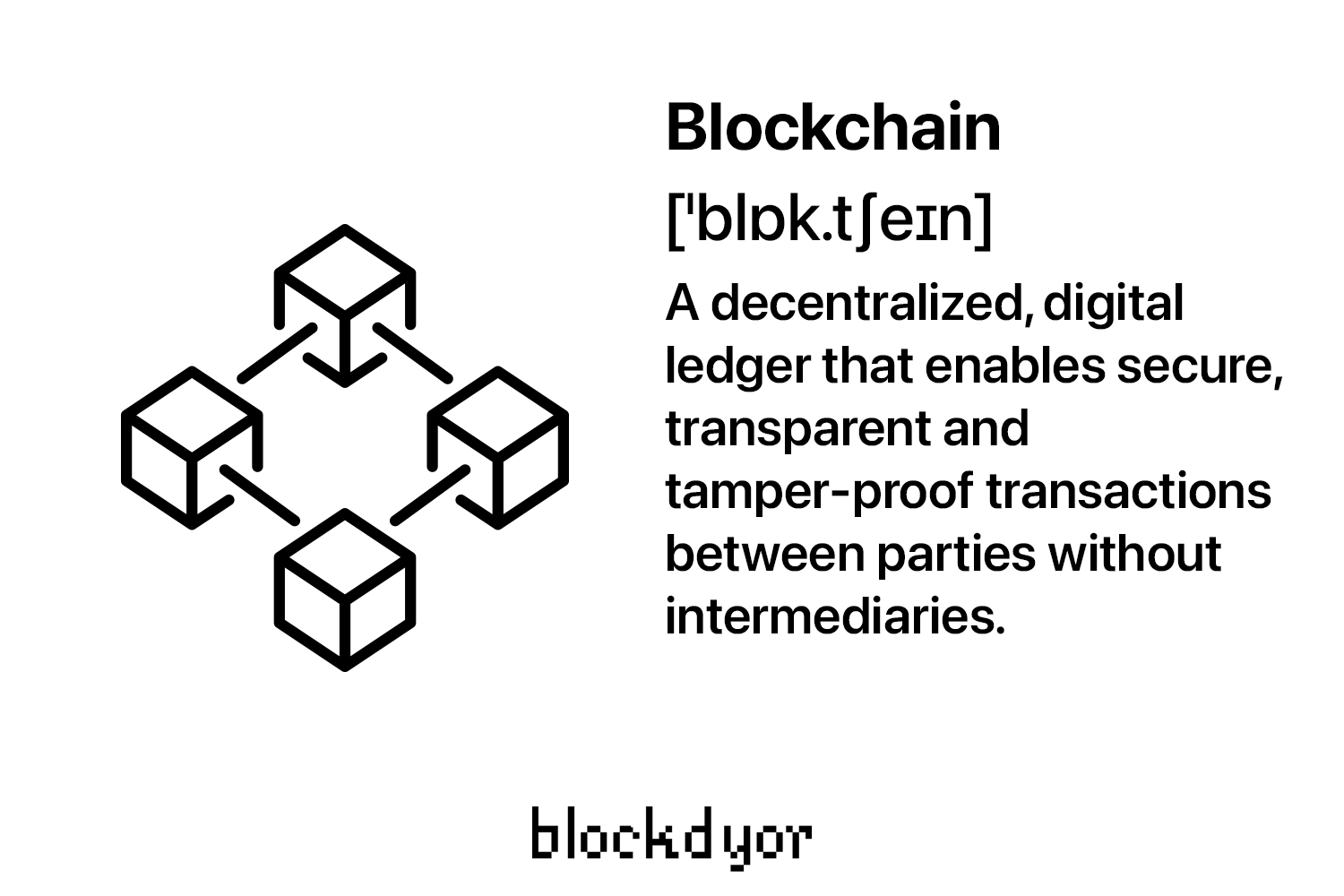

| 🔗 Blockchain | A decentralized, distributed ledger technology that records transactions in a secure and transparent manner |

| 💾 Block | A unit of data that contains a record of several transactions on the blockchain, along with a unique identifier, timestamp, and reference to the previous block |

| 🆕 Genesis Block | The first block on a blockchain, which contains no previous reference and is typically hardcoded into the blockchain's protocol |

| 🏗️ Block Height | The number of blocks in a blockchain, used to determine the current state of the blockchain and ensure the consistency of the ledger |

| 🌐 Decentralization | The distribution of control and decision-making power among a network of nodes, without relying on a central authority or intermediary |

| 🤝 Peer to Peer | A decentralized network architecture where each node can act as both a client and a server, allowing for direct communication and transactions between nodes |

| 💼 Smart Contract | Self-executing contracts with the terms of the agreement between buyer and seller being directly written into lines of code on the blockchain |

| 💻 Solidity | A programming language used to write smart contracts on the Ethereum blockchain |

| 🔒 Immutability | The property of a blockchain that makes data once written to the blockchain cannot be altered or deleted without consensus from the network |

| ⛏️ Mining | The process of verifying and adding new transactions to the blockchain by solving complex mathematical problems, typically done by nodes in exchange for a reward in cryptocurrency |

What is Blockchain?

A blockchain is a unique digital storage system that distinguishes itself from traditional databases through its structure.

The blockchain is basically a shared ledger or distributed database, which can be accessed to nodes inside a network of computers. It is usually used to store electronic data in a secure manner, with the most famous application being in cryptocurrency systems such as the Bitcoin.

What makes a blockchain different from other classic types of databases is the way it structures data. In a blockchain, information is grouped into blocks, each with a predetermined storage capacity. When a certain block receives data, it is closed and connected to the previous block, creating a basically perpetual chain of infos. Any new data is stored in a new block, which is then appended to the existing chain when it becomes full.

In contrast, classic databases store data in tables, whereas blockchains organize it into interconnected blocks. This unique data structure creates timeline of data that is immutable and saved in a decentralized manner. Once a block is filled, it becomes permanent and is added to the timeline, with each block being assigned a precise timestamp when it is added to the chain.

How Does a Blockchain Work?

A blockchain is a digital ledger that is run by a network of computers, also called as nodes. The ledger is essentially a comprehensive record of every single transaction that occurred on the network. Every block in the chain includes a roster of transactions, and once a block becomes a part of the chain, it remains unalterable and cannot be erased.

Validating transactions with Mining

The process of adding a block to the chain is called "mining." Miners use powerful computers to solve complex mathematical puzzles, and the first miner to solve the puzzle gets to add the next block to the chain. This process is called proof-of-work, and it ensures that the transactions on the blockchain are secure and tamper-proof.

Once a block is added to the chain, it is verified by the other nodes on the network to ensure that the transaction is legitimate. This process is called validation, and it helps to prevent fraud and double-spending.

Consensus mechanisms

Consensus mechanisms are the rules that govern how nodes in the network agree on which transactions to add to the blockchain.

There are different types of consensus mechanisms, including Proof of Work (PoW), Proof of Stake (PoS), Delegated Proof of Stake (DPoS), and others.

In PoW, miners compete to solve complex mathematical puzzles, and the first miner to solve the puzzle gets to add the next block to the blockchain.

In PoS and DPoS, validators are chosen based on the amount of cryptocurrency they hold, and they are responsible for validating transactions and adding new blocks to the blockchain.

Consensus mechanisms ensure that the blockchain is secure and tamper-proof, as they prevent any one node from making unauthorized changes to the ledger.

Blockchain Decentralization: What Does It Mean?

Blockchain decentralization refers to the distribution of power and decision-making authority in a blockchain network among its users, rather than relying on a central authority to manage and control the network.

In a decentralized blockchain network, no single entity or individual has control over the network, and all participants have equal rights and responsibilities.

This is achieved through a consensus mechanism, which allows all nodes in the network to agree on the validity of transactions and the state of the blockchain ledger. Decentralization is a fundamental feature of blockchain technology, as it ensures that the network is transparent, immutable, and resistant to censorship or manipulation.

Advantages of Decentralization

Decentralization has several benefits, such as reducing the risk of fraud and corruption, improving transparency and accountability, and fostering innovation and competition. It also enables peer-to-peer transactions without the need for intermediaries, reducing costs and increasing efficiency.

However, achieving true decentralization in a blockchain network can be challenging, as it requires a significant amount of computational power and network resources to maintain the integrity of the network. Additionally, some blockchain networks may have a certain level of centralization due to factors such as mining concentration or governance models.

Examples of decentralized blockchain applications

There are many examples of decentralized blockchain applications across various industries and use cases. Here are some of them:

- Cryptocurrencies - Bitcoin, and (very few) other cryptocurrencies are decentralized blockchain applications that enable peer-to-peer transactions without the need for intermediaries like banks.

- Decentralized Finance (DeFi) - DeFi is a fast-growing area of blockchain technology that offers financial services such as lending, borrowing, and trading without relying on centralized intermediaries. Examples include MakerDAO, Uniswap, and Aave.

- Supply Chain Management - Blockchain technology can be used to create a transparent and secure supply chain management system. Walmart, for instance, is using blockchain to track the origin of its produce.

- Healthcare - Blockchain technology can be used to securely store and share medical records, ensuring that they are accessible to patients and healthcare providers while maintaining patient privacy. Examples include FarmaTrust and Patientory.

- Identity Management - Blockchain technology can be used to create a secure and decentralized identity management system. Civic is an example of a blockchain-based identity management platform.

- Social Media - Some blockchain applications aim to create a decentralized and censorship-resistant social media platform. Examples include Minds and Steemit.

- Gaming - Blockchain technology can be used to create decentralized gaming platforms that allow players to truly own their in-game assets. Examples include Axie Infinity and Gods Unchained.

These are just a few examples of the many decentralized blockchain applications that are being developed and implemented today.

Transparency in Blockchain

Transparency is a crucial part in blockchain technology that helps to build trust and accountability in transactions. By design, blockchain technology ensures transparency through its decentralized and immutable ledger system.

How blockchain technology ensures transparency

Every transaction on a blockchain network is recorded in a distributed ledger that is available for all network participants to view. This means that each participant has access to the same information and can verify the accuracy of transactions. Additionally, blockchain networks use consensus algorithms to ensure that all nodes in the network agree on the validity of transactions, further enhancing transparency.

Benefits of transparency in blockchain

Transparency in blockchain technology offers several benefits. First, it increases accountability, as all parties involved in a transaction can see what is happening and can be held responsible for their actions. Second, it promotes trust, as users can rely on the integrity of the information recorded on the blockchain. Third, it enhances efficiency, as all parties can access the same information and can work together seamlessly.

Use cases of transparent blockchain systems

Transparent blockchain systems have many use cases across various industries. In supply chain management, blockchain technology can be used to track the movement of goods from origin to destination, ensuring that they are produced ethically and sustainably. In healthcare, blockchain technology can be used to create a secure and transparent system for sharing medical records between patients and healthcare providers. In voting systems, blockchain technology can be used to ensure the integrity and transparency of elections. Finally, in financial services, blockchain technology can be used to create a transparent and secure system for lending, borrowing, and trading.

Transparency is a fundamental feature of blockchain technology that enhances accountability, trust, and efficiency. Transparent blockchain systems have numerous applications across various industries, and their adoption is expected to increase in the coming years.

Is the Blockchain Safe?

Blockchain technology is often considere as a secure solution for various industries due to its decentralized and immutable nature. However, like any technology, blockchain is not entirely immune to security threats. Nevertheless, several security features in blockchain technology make it a secure solution for many use cases.

The security features of blockchain technology

One of the primary security features of blockchain technology is its decentralized and distributed nature, which eliminates the risk of a single point of failure.

Each node in a blockchain network holds a copy of the entire ledger, making it challenging to hack or manipulate.

Another essential security feature of blockchain technology is its immutability. Once a transaction is recorded on the blockchain, it cannot be altered, ensuring that the ledger remains tamper-proof.

Cryptography in blockchain

Cryptography is also an essential security feature of blockchain technology. Blockchain networks use advanced cryptographic algorithms to ensure the privacy and security of transactions. Hash functions are used to generate a unique code for each transaction, which is added to the blockchain. These hash functions are irreversible, making it impossible to reconstruct the original data.

Examples of successful blockchain security

Several blockchain applications have successfully implemented security features to protect against hacking and other security threats. For instance, Bitcoin has been operating securely for more than a decade, with no significant security breaches. Ethereum, another blockchain-based platform, has also implemented several security measures, such as smart contracts and gas limits, to prevent malicious activities on its network.

Another example is the Hyperledger Fabric, a blockchain-based framework for enterprise use cases. Hyperledger Fabric offers features such as access control, identity management, and encrypted communication to ensure the security and privacy of transactions.

Blockchain technology offers several security features, including decentralization, immutability, and cryptography, that make it a secure solution for various use cases. While no technology is entirely immune to security threats, blockchain's security features can effectively protect against many potential security breaches.

Blockchain vs. Banks

Blockchain technology is often viewed as a disruptive force in the financial industry, challenging the traditional, old fashioned banking system. Here are some advantages and disadvantages of blockchain compared to traditional banking systems, as well as the potential impact of blockchain on the banking industry.

Advantages of blockchain compared to traditional banking systems

- Decentralization: Unlike traditional banking systems that are centralized, blockchain technology is decentralized, making it more resistant to fraud, hacking, and other security threats.

- Transparency: Blockchain technology offers transparency, as all transactions are recorded on a public ledger that can be accessed by all participants.

- Speed: Blockchain technology enables near-instantaneous transactions, eliminating the need for intermediaries and reducing the time required to settle transactions.

- Cost: Blockchain technology can be more cost-effective than traditional banking systems, as it eliminates intermediaries, reduces administrative costs, and improves operational efficiency.

Disadvantages of blockchain compared to traditional banking systems

- Limited adoption: While blockchain technology is gaining traction, it still has limited adoption compared to traditional banking systems. However, this might change in the future as more and more people use underlying technologies such as Bitcoin.

- Regulatory challenges: Blockchain technology operates in a legal gray area, as regulations have not yet caught up with its potential use cases.

- Complexity: Blockchain technology can be complex, requiring technical expertise to develop and implement.

The potential impact of blockchain on the banking industry

Blockchain technology has the potential to revolutionize the banking industry by offering greater security, transparency, and efficiency.

For instance, blockchain technology can be used to create a secure and transparent system for payments, reducing the need for intermediaries and lowering transaction costs. It can also be used to create a decentralized lending and borrowing system, offering greater access to credit and reducing the risk of default.

However, the adoption of blockchain technology in the banking industry also poses challenges. For instance, banks may need to invest in new infrastructure and hire specialized personnel to develop and implement blockchain solutions. Additionally, blockchain technology may disrupt existing business models, leading to job losses and other challenges.

In conclusion, blockchain technology offers several advantages over traditional banking systems, including decentralization, transparency, speed, and cost-effectiveness. However, its adoption also poses challenges, and its impact on the banking industry remains to be seen.

Pros and Cons of Blockchain

| Pros | Cons |

|---|---|

| ✅ Decentralized control | ❌ Energy consumption and environmental impact |

| ✅ Increased transparency | ❌ Scalability and speed |

| ✅ Improved security | ❌ Regulation and legal challenges |

| ✅ Reduction in transaction costs | ❌ Complexity and technical knowledge required |

| ✅ Improved efficiency | ❌ Resistance to change and adoption challenges |

| ✅ Enhanced traceability | ❌ Potential for human error in smart contracts |

| ✅ Potential for innovation and new business models | ❌ Potential for illicit activities and black market transactions |

Bottom line

In conclusion, blockchain technology has the potential to revolutionize many industries and transform the way we live and work. Thanks to its unique features such as decentralization, immutability, and transparency, blockchain can address issues of trust, security, and efficiency in various domains such as finance, supply chain management, healthcare, and more.

In this guide, we discussed the fundamental concepts of blockchain technology, its components, and its various applications. We explored the benefits and limitations of blockchain and how it differs from traditional centralized systems. We also examined some of the challenges and risks associated with blockchain implementation, including scalability, interoperability, and regulatory compliance.

Looking ahead, the future of blockchain technology is promising. With ongoing research and development, we can expect to see new and innovative use cases emerge, such as digital identity management, decentralized finance (DeFi), and non-fungible tokens (NFTs). Additionally, blockchain can play a significant role in shaping the future of the internet and the concept of Web3, where users have more control and ownership over their data and digital assets.

In conclusion, the potential impact of blockchain technology on society is significant, and it will undoubtedly shape the way we interact with each other and conduct business. As the technology continues to evolve and mature, it is crucial to stay informed and explore its possibilities for innovation and growth.